|

USE OF PROCEEDS We estimate that the net proceeds to us from the sale of shares of our common stock in this offering will be approximately $ , based upon the assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. If the underwriters’ option to purchase additional shares of our common stock from us is exercised in full, we estimate that the net proceeds to us would be approximately $ , after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. Each $1.00 increase or decrease in the assumed initial public offering price of $ per share would increase or decrease the net proceeds that we receive from this offering by approximately $ , assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting the estimated underwriting discounts and commissions payable by us. Similarly, each increase or decrease of one million in the number of shares of our common stock offered by us would increase or decrease the net proceeds that we receive from this offering by approximately $ , assuming the assumed initial public offering price remains the same and after deducting the estimated underwriting discounts and commissions payable by us. The principal purposes of this offering are to increase our capitalization and financial flexibility, create a public market for our common stock and enable access to the public equity markets for us and our stockholders. We intend to use the net proceeds from this offering for general corporate purposes, including working capital, operating expenses and capital expenditures. We anticipate making capital expenditures in 2013 of approximately $225 million to $275 million, and we may use a portion of the net proceeds to fund our anticipated capital expenditures. We also may use a portion of the net proceeds to satisfy our anticipated tax withholding and remittance obligations related to the settlement of our outstanding Pre-2013 RSUs, or we may choose to allow our employees who are not executive officers holding such awards to sell shares of our common stock in the public market to satisfy their income tax obligations related to the vesting and settlement of such awards. Based on the number of Pre-2013 RSUs outstanding as of June 30, 2013 for which the service condition had been satisfied on that date, and assuming (i) the performance condition had been satisfied on that date, (ii) we choose to undertake a net settlement of all of our Pre-2013 RSUs and (iii) that the price of our common stock at the time of settlement was equal to $ , which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, we estimate that this tax obligation on the initial settlement date would be approximately $ in the aggregate. The amount of this obligation could be higher or lower, depending on the price of shares of our common stock on the initial settlement date for the Pre-2013 RSUs. Additionally, we may use a portion of the net proceeds to acquire businesses, products, services or technologies. However, except for our proposed acquisition of MoPub in exchange for shares of our common stock, we do not have agreements or commitments for any material acquisitions at this time. We cannot specify with certainty the particular uses of the net proceeds that we will receive from this offering. Accordingly, we will have broad discretion in using these proceeds. Pending the use of proceeds from this offering as described above, we plan to invest the net proceeds that we receive in this offering in short-term and long-term interest-bearing obligations, including government and investment-grade debt securities and money market funds. DIVIDEND POLICY We have never declared or paid any cash dividends on our capital stock. We currently intend to retain any future earnings and do not expect to pay any dividends in the foreseeable future. Any future determination to declare cash dividends will be made at the discretion of our board of directors, subject to applicable laws, and will depend on a number of factors, including our financial condition, results of operations, capital requirements, contractual restrictions, general business conditions and other factors that our board of directors may deem relevant. 51

Table of ContentsCAPITALIZATION The following table sets forth cash and cash equivalents, as well as our capitalization, as of June 30, 2013 as follows:

| | Ÿ | | on a pro forma basis, giving effect to (i) the automatic conversion of all outstanding shares of our Class A junior preferred stock and our convertible preferred stock into an aggregate of 333,099,000 shares of our common stock, which conversion will occur immediately prior to the completion of this offering, as if such conversion had occurred on June 30, 2013, (ii) the resulting reclassification of the restricted Class A junior preferred stock of $6.7 million and preferred stock warrant liability of $2.0 million from other long-term liabilities to additional paid-in capital, (iii) stock-based compensation expense of $329.6 million associated with Pre-2013 RSUs for which the service condition was satisfied as of June 30, 2013, and which we expect to record upon completion of this offering, as described in footnote (1) below and (iv) the filing and effectiveness of our amended and restated certificate of incorporation in Delaware; and |

| | Ÿ | | on a pro forma as adjusted basis, giving effect to the pro forma adjustments set forth above and the sale and issuance by us of shares of our common stock in this offering, based upon the assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

You should read this table together with our consolidated financial statements and related notes, and the sections titled “Selected Consolidated Financial and Other Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” that are included elsewhere in this prospectus.

| | | | | | | | | | | | | | | | As of June 30, 2013 | | | | | Actual | | | Pro

Forma(1) | | | Pro Forma

as

Adjusted(2) | | | | | (In thousands, except share and

per share data) | | Cash, cash equivalents and short-term investments | | $ | 375,058 | | | $ | 375,058 | | | $ | | | | |

|

| | |

|

| | |

|

| | Restricted Class A junior preferred stock and preferred stock warrant liabilities included in other long term liabilities | | | 8,735 | | | | — | | | | | | Redeemable Class A junior preferred stock, par value $0.000005 per share: 15,000,000 shares authorized, 3,523,675 issued and outstanding, actual; no shares authorized, issued and outstanding, pro forma and pro forma as adjusted | | | 37,106 | | | | — | | | | | | Convertible preferred stock, par value $0.000005 per share: 329,691,856 shares authorized, 329,575,325 issued and outstanding, actual; no shares authorized, issued and outstanding, pro forma and pro forma as adjusted | | | 835,430 | | | | — | | | | | | Stockholders’ equity (deficit): | | | | | | | | | | | | | Preferred stock, par value $0.000005 per share: no shares authorized, issued and outstanding, actual; shares authorized, no shares issued and outstanding, pro forma and pro forma as adjusted | | | — | | | | — | | | | | | Common stock, par value $0.000005 per share: 600,000,000 shares authorized, 139,514,753 shares issued and outstanding, actual; shares authorized, 472,613,753 shares issued and outstanding, pro forma and shares authorized, shares issued and outstanding, pro forma as adjusted | | | 1 | | | | 2 | | | | | | Additional paid-in capital | | | 254,831 | | | | 1,465,733 | | | | | | Accumulated other comprehensive loss | | | (653 | ) | | | (653 | ) | | | | | Accumulated deficit | | | (418,554 | ) | | | (748,186 | ) | | | | | | |

|

| | |

|

| | |

|

| | Total stockholders’ equity (deficit) | | | (164,375 | ) | | | 716,896 | | | | | | | |

|

| | |

|

| | |

|

| | Total capitalization | | $ | 716,896 | | | $ | 716,896 | | | $ | | | | |

|

| | |

|

| | |

|

| |

52

Table of Contents

(1) | The pro forma data as of June 30, 2013 gives effect to stock-based compensation expense of $329.6 million associated with Pre-2013 RSUs for which the service condition was satisfied as of June 30, 2013 and which we expect to record upon completion of this offering, as further described in “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies and Estimates—Stock-Based Compensation.” The pro forma adjustment related to stock-based compensation expense of $329.6 million has been reflected as an increase to additional paid-in capital and accumulated deficit. We estimate that an aggregate of approximately million shares underlying Pre-2013 RSUs outstanding as of June 30, 2013 will vest and settle on in connection with the satisfaction of the performance condition to their vesting, resulting in the net issuance of an aggregate of approximately million shares to the holders if we choose to undertake a net settlement of all of these awards rather than allowing our employees who are not executive officers to sell shares of our common stock in the public market to satisfy their income tax obligations related to the vesting and settlement of such awards. These shares have not been included in our pro forma or pro forma as adjusted shares outstanding. |

(2) | Each $1.00 increase or decrease in the assumed initial public offering price of our common stock of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, would increase or decrease, as applicable, the amount of our pro forma as adjusted cash and cash equivalents, additional paid-in capital and total stockholders’ equity by approximately $ , assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions payable by us. An increase or decrease of 1.0 million shares in the number of shares offered by us would increase or decrease, as applicable, the amount of our pro forma as adjusted cash and cash equivalents, additional paid-in capital and total stockholders’ equity by approximately $ , assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions payable by us. |

If the underwriters’ option to purchase additional shares of our common stock from us were exercised in full, pro forma as adjusted cash and cash equivalents, additional paid-in capital, total stockholders’ equity and shares outstanding as of June 30, 2013 would be $ , $ , $ and $ , respectively. The pro forma and pro forma as adjusted columns in the table above are based on 472,613,753 shares of our common stock (including preferred stock on an as-converted basis) outstanding as of June 30, 2013, and exclude the following:

| | Ÿ | | 44,157,061 shares of our common stock issuable upon the exercise of options to purchase shares of our common stock outstanding as of June 30, 2013, with a weighted-average exercise price of $1.82 per share; |

| | Ÿ | | 59,913,992 shares of our common stock subject to RSUs outstanding as of June 30, 2013; |

| | Ÿ | | 116,512 shares of our common stock, on an as-converted basis, issuable upon the exercise of a warrant to purchase convertible preferred stock outstanding as of June 30, 2013, with an exercise price of $0.34 per share; |

| | Ÿ | | 27,002,040 shares of our common stock subject to RSUs granted after June 30, 2013; |

| | Ÿ | | up to 14,791,464 shares of our common stock issuable upon completion of our acquisition of MoPub; and |

| | Ÿ | | shares of our common stock reserved for future issuance under our equity compensation plans which will become effective prior to the completion of this offering, consisting of: |

| | Ÿ | | shares of our common stock reserved for future issuance under our 2013 Plan; |

| | Ÿ | | 7,814,902 shares of our common stock reserved for future issuance under our 2007 Plan (after giving effect to an increase of 20,000,000 shares of our common stock reserved for issuance under our 2007 Plan after June 30, 2013 and the grant of 27,002,040 shares of our common stock subject to RSUs granted after June 30, 2013), which number of shares will be added to the shares of our common stock to be reserved under our 2013 Plan upon its effectiveness; and |

| | Ÿ | | shares of our common stock reserved for future issuance under our ESPP. |

Our 2013 Plan and ESPP each provide for annual automatic increases in the number of shares reserved thereunder, and our 2013 Plan also provides for increases to the number of shares that may be granted thereunder based on shares under our 2007 Plan that expire, are forfeited or otherwise repurchased by us, as more fully described in the section titled “Executive Compensation—Employee Benefit and Stock Plans.” 53

Table of ContentsDILUTION If you invest in our common stock in this offering, your ownership interest will be diluted to the extent of the difference between the initial public offering price per share of our common stock and the pro forma as adjusted net tangible book value per share of our common stock immediately after this offering. Net tangible book value dilution per share to new investors represents the difference between the amount per share paid by purchasers of shares of our common stock in this offering and the pro forma as adjusted net tangible book value per share of our common stock immediately after completion of this offering. Net tangible book value per share is determined by dividing our total tangible assets less our total liabilities by the number of shares of our common stock outstanding. Our historical net tangible deficit as of June 30, 2013 was $342.5 million, or $2.46 per share. Our pro forma net tangible book value as of June 30, 2013 was $538.7 million, or $1.14 per share, based on the total number of shares of our common stock outstanding as of June 30, 2013, after giving effect to the automatic conversion of all outstanding shares of our Class A junior preferred stock and our convertible preferred stock as of June 30, 2013 into an aggregate of 333,099,000 shares of our common stock, which conversion will occur immediately prior to the completion of this offering, and the resulting reclassification of the restricted Class A junior preferred stock and preferred stock warrant liability from other long-term liabilities to additional paid-in capital. After giving effect to the sale by us of shares of our common stock in this offering at the assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us, our pro forma as adjusted net tangible book value as of June 30, 2013 would have been $ million, or $ per share. This represents an immediate increase in pro forma net tangible book value of $ per share to our existing stockholders and an immediate dilution in pro forma net tangible book value of $ per share to investors purchasing shares of our common stock in this offering at the assumed initial public offering price. The following table illustrates this dilution:

| | | | | | | | | Assumed initial public offering price per share | | | | | | $ | | | Pro forma net tangible book value (deficit) per share as of June 30, 2013 | | $ | 1.14 | | | | | | Increase in pro forma net tangible book value (deficit) per share attributable to new investors in this offering | | | | | | | | | | |

|

| | | | | | Pro forma as adjusted net tangible book value per share immediately after this offering | | | | | | | | | | | | | | |

|

| | Dilution in pro forma net tangible book value per share to new investors in this offering | | | | | | $ | | | | | | | | |

|

| |

Each $1.00 increase or decrease in the assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, would increase or decrease, as applicable, our pro forma as adjusted net tangible book value per share to new investors by $ , and would increase or decrease, as applicable, dilution per share to new investors in this offering by $ , assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. Similarly, each increase or decrease of 1.0 million shares in the number of shares offered by us would increase or decrease, as applicable, our pro forma as adjusted net tangible book value by approximately $ per share and increase or decrease, as applicable, the dilution to new investors by $ per share, assuming the assumed initial public offering price remains the same, and after deducting underwriting discounts and commissions and estimated offering expenses payable by us. 54

Table of ContentsIf the underwriters’ option to purchase additional shares of our common stock from us is exercised in full, the pro forma as adjusted net tangible book value per share of our common stock, as adjusted to give effect to this offering, would be $ per share, and the dilution in pro forma net tangible book value per share to new investors in this offering would be $ per share. The following table presents, as of June 30, 2013, after giving effect to the automatic conversion of all outstanding shares of our Class A junior preferred stock and our convertible preferred stock into our common stock immediately prior to the completion of this offering, the differences between the existing stockholders and the new investors purchasing shares of our common stock in this offering with respect to the number of shares purchased from us, the total consideration paid or to be paid to us, which includes net proceeds received from the issuance of our common stock and preferred stock, cash received from the exercise of stock options and the average price per share paid or to be paid to us at the assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, before deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us:

| | | | | | | | | | | | | | | | | | | | | | Shares Purchased | | | Total Consideration | | | Average

Price Per

Share | | | | | Number | | Percent | | | Amount | | | Percent | | | Existing stockholders | | | | | | % | | $ | | | | | | % | | $ | | | New investors | | | | | | | | | | | | | | | | | | | | |

| |

|

| | |

|

| | |

|

| | | | | | Totals | | | | | 100 | % | | $ | | | | | 100 | % | | | | | | |

| |

|

| | |

|

| | |

|

| | | | | |

Each $1.00 increase or decrease in the assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, would increase or decrease, as applicable, the total consideration paid by new investors and total consideration paid by all stockholders by approximately $ , assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. Except as otherwise indicated, the above discussion and tables assume no exercise of the underwriters’ option to purchase additional shares of our common stock from us. If the underwriters’ option to purchase additional shares of our common stock were exercised in full, our existing stockholders would own % and our new investors would own % of the total number of shares of our common stock outstanding upon the completion of this offering. The number of shares of our common stock that will be outstanding after this offering is based on 472,613,753 shares of our common stock (including preferred stock on an as-converted basis) outstanding as of June 30, 2013, and excludes:

| | Ÿ | | 44,157,061 shares of our common stock issuable upon the exercise of options to purchase shares of our common stock outstanding as of June 30, 2013, with a weighted-average exercise price of $1.82 per share; |

| | Ÿ | | 59,913,992 shares of our common stock subject to RSUs outstanding as of June 30, 2013; |

| | Ÿ | | 116,512 shares of our common stock, on an as-converted basis, issuable upon the exercise of a warrant to purchase convertible preferred stock outstanding as of June 30, 2013, with an exercise price of $0.34 per share; |

| | Ÿ | | 27,002,040 shares of our common stock subject to RSUs granted after June 30, 2013; |

| | Ÿ | | up to 14,791,464 shares of our common stock issuable upon completion of our acquisition of MoPub; and |

55

Table of Contents| | Ÿ | | shares of our common stock reserved for future issuance under our equity compensation plans which will become effective prior to the completion of this offering, consisting of: |

| | Ÿ | | shares of our common stock reserved for future issuance under our 2013 Plan; |

| | Ÿ | | 7,814,902 shares of our common stock reserved for future issuance under our 2007 Plan (after giving effect to an increase of 20,000,000 shares of our common stock reserved for issuance under our 2007 Plan after June 30, 2013 and the grant of 27,002,040 shares of our common stock subject to RSUs granted after June 30, 2013), which number of shares will be added to the shares of our common stock to be reserved under our 2013 Plan upon its effectiveness; and |

| | Ÿ | | shares of our common stock reserved for future issuance under our ESPP. |

Our 2013 Plan and ESPP each provide for annual automatic increases in the number of shares reserved thereunder, and our 2013 Plan also provides for increases to the number of shares that may be granted thereunder based on shares under our 2007 Plan that expire, are forfeited or otherwise repurchased by us, as more fully described in the section titled “Executive Compensation—Employee Benefit and Stock Plans.” To the extent that any outstanding options to purchase our common stock or a warrant to purchase convertible preferred stock are exercised, RSUs are settled or new awards are granted under our equity compensation plans, there will be further dilution to investors participating in this offering. 56

Table of ContentsSELECTED CONSOLIDATED FINANCIAL AND OTHER DATA The following selected consolidated statement of operations data for the years ended December 31, 2010, 2011 and 2012 and the consolidated balance sheet data as of December 31, 2011 and 2012 have been derived from our audited consolidated financial statements included elsewhere in this prospectus. The consolidated balance sheet data as of December 31, 2010 has been derived from our audited consolidated financial statements not included in this prospectus. The selected consolidated statement of operations data for the six months ended June 30, 2012 and 2013 and the consolidated balance sheet data as of June 30, 2013 have been derived from our unaudited interim consolidated financial statements included elsewhere in this prospectus. The unaudited interim consolidated financial statements have been prepared on the same basis as the audited financial statements and reflect, in the opinion of management, all adjustments, of a normal, recurring nature that are necessary for a fair statement of the unaudited interim consolidated financial statements. Our historical results are not necessarily indicative of the results that may be expected in the future and the results in the six months ended June 30, 2013 are not necessarily indicative of results to be expected for the full year or any other period. You should read the following selected consolidated financial and other data below in conjunction with the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes included elsewhere in this prospectus.

| | | | | | | | | | | | | | | | | | | | | | | | Year Ended December 31, | | | Six Months Ended

June 30, | | | | | 2010 | | | 2011 | | | 2012 | | | 2012 | | | 2013 | | | | | (In thousands, except per share data) | | Consolidated Statement of Operations Data: | | | | | | | | | | | | | | | | | | | | | Revenue | | $ | 28,278 | | | $ | 106,313 | | | $ | 316,933 | | | $ | 122,359 | | | $ | 253,635 | | Costs and expenses(1) | | | | | | | | | | | | | | | | | | | | | Cost of revenue | | | 43,168 | | | | 61,803 | | | | 128,768 | | | | 58,157 | | | | 91,828 | | Research and development | | | 29,348 | | | | 80,176 | | | | 119,004 | | | | 46,345 | | | | 111,837 | | Sales and marketing | | | 6,289 | | | | 25,988 | | | | 86,551 | | | | 34,105 | | | | 77,697 | | General and administrative | | | 16,952 | | | | 65,757 | | | | 59,693 | | | | 30,758 | | | | 35,096 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Total costs and expenses | | | 95,757 | | | | 233,724 | | | | 394,016 | | | | 169,365 | | | | 316,458 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Loss from operations | | | (67,479 | ) | | | (127,411 | ) | | | (77,083 | ) | | | (47,006 | ) | | | (62,823 | ) | Interest income (expense), net | | | 55 | | | | (805 | ) | | | (2,486 | ) | | | (890 | ) | | | (2,746 | ) | Other income (expense), net | | | (117 | ) | | | (1,530 | ) | | | 399 | | | | (12 | ) | | | (2,548 | ) | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Loss before income taxes | | | (67,541 | ) | | | (129,746 | ) | | | (79,170 | ) | | | (47,908 | ) | | | (68,117 | ) | Provision (benefit) for income taxes | | | (217 | ) | | | (1,444 | ) | | | 229 | | | | 1,196 | | | | 1,134 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Net loss | | $ | (67,324 | ) | | $ | (128,302 | ) | | $ | (79,399 | ) | | $ | (49,104 | ) | | $ | (69,251 | ) | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Deemed dividend to investors in relation to the tender offer | | | — | | | | 35,816 | | | | — | | | | — | | | | — | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Net loss attributable to common stockholders | | $ | (67,324 | ) | | $ | (164,118 | ) | | $ | (79,399 | ) | | $ | (49,104 | ) | | $ | (69,251 | ) | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Weighted-average shares used to compute net loss per share attributable to common stockholders: | | | | | | | | | | | | | | | | | | | | | Basic and diluted | | | 75,992 | | | | 102,544 | | | | 117,401 | | | | 114,825 | | | | 129,853 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Net loss per share attributable to common stockholders: | | | | | | | | | | | | | | | | | | | | | Basic and diluted | | $ | (0.89 | ) | | $ | (1.60 | ) | | $ | (0.68 | ) | | $ | (0.43 | ) | | $ | (0.53 | ) | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Pro forma net loss per share attributable to common stockholders (unaudited) 2) 2) | | | | | | | | | | | | | | | | | | | | | Basic and diluted | | | | | | | | | | $ | (0.18 | ) | | | | | | $ | (0.15 | ) | | | | | | | | | | |

|

| | | | | | |

|

| | | | | | | | Other Financial Information3) | | | | | | | | | | | | | | | | | | | | | Adjusted EBITDA | | $ | (51,184 | ) | | $ | (42,835 | ) | | $ | 21,164 | | | $ | 670 | | | $ | 21,392 | | Non-GAAP net loss | | $ | (54,066 | ) | | $ | (65,533 | ) | | $ | (35,191 | ) | | $ | (22,232 | ) | | $ | (26,888 | ) |

57

Table of Contents

(1) | Costs and expenses include stock-based compensation expense as follows: |

| | | | | | | | | | | | | | | | | | | | | | | | Year Ended December 31, | | | Six Months Ended

June 30, | | | | | 2010 | | | 2011 | | | 2012 | | | 2012 | | | 2013 | | | | | (In thousands) | | | | | | | | | | Cost of revenue | | $ | 200 | | | $ | 1,820 | | | $ | 800 | | | $ | 420 | | | $ | 1,955 | | Research and development | | | 3,409 | | | | 33,559 | | | | 12,622 | | | | 6,291 | | | | 24,197 | | Sales and marketing | | | 249 | | | | 1,553 | | | | 1,346 | | | | 620 | | | | 4,614 | | General and administrative | | | 2,073 | | | | 23,452 | | | | 10,973 | | | | 8,796 | | | | 4,802 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Total stock-based compensation | | $ | 5,931 | | | $ | 60,384 | | | $ | 25,741 | | | $ | 16,127 | | | $ | 35,568 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| |

(2) | See Note 9 to our consolidated financial statements for an explanation of the calculations of our pro forma net loss per share attributable to common stockholders. |

(3) | See the sections titled “Prospectus Summary—Summary Consolidated Financial and Other Data—Non-GAAP Financial Measures” for additional information and a reconciliation of net loss to Adjusted EBITDA and net loss to non-GAAP net loss. |

| | | | | | | | | | | | | | | | | | | | Year Ended December 31, | | | As of

June 30,

2013 | | | | | 2010 | | | 2011 | | | 2012 | | | | | | (In thousands) | | | | | | | | | | | | | | (Unaudited) | | Consolidated Balance Sheet Data: | | | | | | | | | | | | | | | | | Cash and cash equivalents | | $ | 134,253 | | | $ | 218,996 | | | $ | 203,328 | | | $ | 164,509 | | Short-term investments | | | 43,484 | | | | 330,543 | | | | 221,528 | | | | 210,549 | | Working capital | | | 167,088 | | | | 548,324 | | | | 444,587 | | | | 382,820 | | Property and equipment, net | | | 26,385 | | | | 61,983 | | | | 185,574 | | | | 242,553 | | Total assets | | | 224,473 | | | | 720,675 | | | | 831,568 | | | | 964,059 | | Total liabilities | | | 35,432 | | | | 87,391 | | | | 207,204 | | | | 255,898 | | Redeemable convertible preferred stock | | | — | | | | 49 | | | | 37,106 | | | | 37,106 | | Convertible preferred stock | | | 279,534 | | | | 835,073 | | | | 835,430 | | | | 835,430 | | Total stockholders’ deficit | | $ | (90,493 | ) | | $ | (201,838 | ) | | $ | (248,172 | ) | | $ | (164,375 | ) |

58

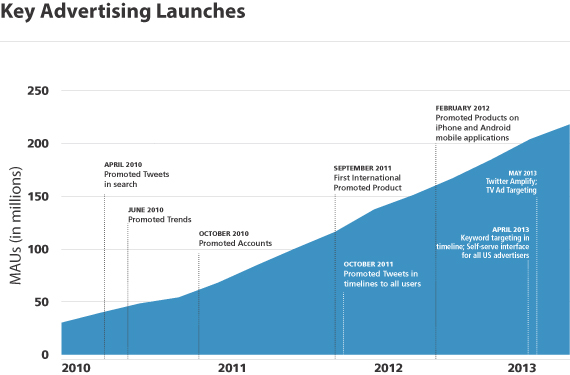

Table of ContentsMANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS The following discussion and analysis of our financial condition and results of operations should be read in conjunction with the section titled “Selected Consolidated Financial and Other Data” and the consolidated financial statements and related notes thereto included elsewhere in this prospectus. This discussion contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those discussed below. Factors that could cause or contribute to such differences include, but are not limited to, those identified below and those discussed in the section titled “Risk Factors” included elsewhere in this prospectus. Overview Twitter is a global platform for public self-expression and conversation in real time. Our platform is unique in its simplicity: Tweets are limited to 140 characters of text. This constraint makes it easy for anyone to quickly create, distribute and discover content that is consistent across our platform and optimized for mobile devices. As a result, Tweets drive a high velocity of information exchange that makes Twitter uniquely “live.” We have already achieved significant global scale, and we continue to grow. We have more than 215 million MAUs spanning nearly every country. Our users include millions of people from around the world, as well as influential individuals and organizations, such as world leaders, government officials, celebrities, athletes, journalists, sports teams, media outlets and brands. Our users create approximately 500 million Tweets every day. The value we create for our users is enhanced by our platform partners and advertisers. Millions of platform partners, which include publishers, media outlets and developers, have integrated with Twitter, adding value to our user experience by contributing content to our platform, broadly distributing content from our platform across their properties and using Twitter content and tools to enhance their websites and applications. In addition, advertisers use our Promoted Products to promote their brands, products and services, amplify their visibility and reach, and complement and extend the conversation around their advertising campaigns. Although we do not generate revenue directly from users or platform partners, we benefit from network effects where more activity on Twitter results in the creation and distribution of more content, which attracts more users, platform partners and advertisers, resulting in a virtuous cycle of value creation. We generate the substantial majority of our revenue from the sale of advertising services, with the balance coming from data licensing arrangements. We generate nearly all of our advertising revenue through the sale of our three Promoted Products: Promoted Tweets, Promoted Accounts and Promoted Trends. The substantial majority of our advertising revenue is generated on a pay-for-performance basis, which means advertisers are only charged when a user engages with their ad, creating an attractive value proposition for our advertisers. We launched our first Promoted Products in mid-2010 in the United States by introducing Promoted Tweets in search results and Promoted Trends. Since that time, we have expanded our Promoted Products to add Promoted Accounts and extended our Promoted Products across our platform and to additional geographies. We generate advertising sales in the United States and certain other geographies through our direct sales force, as well as through our self-serve advertising platform. We introduced Promoted Products on our iOS and Android mobile applications in February 2012. Over 65% of our advertising revenue was generated from mobile devices in the three months ended June 30, 2013. 59

Table of ContentsOur international revenue was $53.0 million and $62.8 million in 2012 and the six months ended June 30, 2013, respectively, representing 17% and 25% of our total revenue for those periods, respectively. We launched Promoted Products in selected international markets in the third quarter of 2011, and we expect to continue to launch our Promoted Products in additional markets over time. We have recently focused our international spending on sales support and marketing activities in specific countries, including Australia, Brazil, Canada, Japan and the United Kingdom. In certain international geographies where we have not invested to build a local sales force, we rely on resellers that serve as outside sales agents for the sale of our Promoted Products. In the six months ended June 30, 2013, we and our resellers sold our Promoted Products to advertisers in over 20 countries outside of the United States. We record advertising revenue based on the billing location of our advertisers, rather than the location of our users. We are headquartered in San Francisco, California, and have offices in over 15 cities around the world. Key Milestones We have developed our advertising services through the introduction of numerous products and services, including:

60

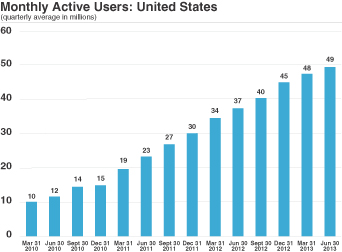

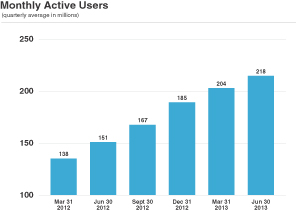

Table of ContentsKey Metrics We review a number of metrics, including the following key metrics, to evaluate our business, measure our performance, identify trends affecting our business, formulate business plans and make strategic decisions: Monthly Active Users (MAUs). We define MAUs as Twitter users who logged in and accessed Twitter through our website, mobile website, desktop or mobile applications, SMS or registered third-party applications or websites in the 30-day period ending on the date of measurement. Average MAUs for a period represent the average of the MAUs at the end of each month during the period. In the discussion of our results of operations we compare average MAUs for the last three months of each period discussed in such comparison. MAUs are a measure of the size of our active user base. In the three months ended June 30, 2013, we had 218.3 million average MAUs, which represents an increase of 44% from the three months ended June 30, 2012. In the three months ended June 30, 2013, we had 49.2 million average MAUs in the United States and 169.1 million average MAUs in the rest of the world, which represent increases of 35% and 47%, respectively, from the three months ended June 30, 2012. For additional information on how we calculate the number of MAUs and factors that can affect this metric, see the section titled “Industry Data and Company Metrics.”

61

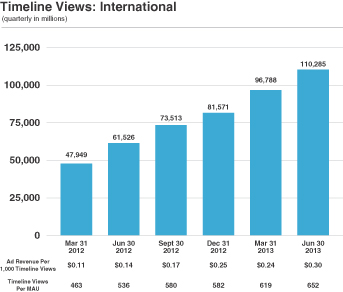

Table of ContentsTimeline Views, Timeline Views Per MAU and Advertising Revenue Per Timeline View. We define timeline views as the total number of timelines requested when registered users visit Twitter, refresh a timeline or view search results while logged in on our website, mobile website or desktop or mobile applications (excluding our TweetDeck and Mac clients, as we do not fully track this data). We believe that timeline views and timeline views per MAU are measures of user engagement. Timeline views per MAU are calculated by dividing the total timeline views for the period by the average MAUs for the last three months of such period. In the three months and six months ended June 30, 2013, we had 150.9 billion and 287.2 billion timeline views, respectively, which represent increases of 69% and 79% from the three months and six months ended June 30, 2012, respectively. In the three months and six months ended June 30, 2013, we had 40.6 billion and 80.2 billion timeline views in the United States, respectively, which represent increases of 45% and 57% from the three months and six months ended June 30, 2012, respectively. In the three months and six months ended June 30, 2013, we had 110.3 billion and 207.1 billion timeline views in the rest of the world, respectively, which represent increases of 79% and 89% from the three months and six months ended June 30, 2012, respectively. In the three months ended June 30, 2013, we had 691 timeline views per MAU, which represents an increase of 17% from the three months ended June 30, 2012. In the three months ended June 30, 2013, we had 825 timeline views per MAU in the United States and 652 timeline views per MAU in the rest of the world, which represent increases of 8% and 22% from the three months ended June 30, 2012, respectively. For additional information on how we calculate the number of timeline views and factors that can affect this metric, see the section titled “Industry Data and Company Metrics.” We define advertising revenue per timeline view as advertising revenue per 1,000 timeline views during the applicable period. We believe that advertising revenue per timeline view is a measure of our ability to monetize our platform. In the three months ended June 30, 2013, our advertising revenue per timeline view was $0.80, which represents a 26% increase from the three months ended June 30, 2012. In the three months ended June 30, 2013, our advertising revenue per timeline view in the United States was $2.17 and our advertising revenue per timeline view in the rest of the world was $0.30, which represent increases of 26% and 111% from the three months ended June 30, 2012, respectively. We record advertising revenue based on the billing location of our advertisers, rather than the location of our users. 62

Table of Contents

Factors Affecting Our Future Performance User Growth, User Engagement and Monetization. User growth trends reflected in the number of MAUs, user engagement trends reflected in timeline views and timeline views per MAU and monetization trends reflected in advertising revenue per timeline view are key factors that affect our revenue. As our user base and the level of engagement of our users grow, we believe the potential to increase our revenue grows. User Growth. We have experienced significant growth in our number of users over the last several years. In general, a higher proportion of Internet users in the United States uses Twitter than Internet users in other countries. Accordingly, in the future we expect our user growth rate in certain international markets, such as Argentina, France, Japan, Russia, Saudi Arabia and South Africa, to continue to be higher than our user growth rate in the United States. However, we expect to face challenges in entering some markets, such as China, where access to Twitter is blocked, as well as certain other countries that have intermittently restricted access to Twitter. Restrictions or 63

Table of Contentslimitations on access to Twitter may adversely impact our ability to increase the size of our user base and generate additional revenue in certain markets. Our user base continues to grow. Although we do not separately track whether an MAU has only used Twitter on a desktop or on a mobile device, the usage of our mobile applications continues to grow. In the three months ended June 30, 2013, 75% of our average MAUs accessed Twitter from a mobile device, compared to 66% in the three months ended June 30, 2012. We may face challenges in increasing the size of our user base, including, among others, competition from alternative products and services, a decline in the number of influential users on Twitter or a perceived decline in the quality of content available on Twitter. We intend to drive growth in our user base by continuing to demonstrate the value and usefulness of our products and services to potential new users, and by introducing new products, services and features. We anticipate that our user growth rate will slow over time as the size of our user base increases. To the extent our user growth or user growth rate slows, our revenue growth will become increasingly dependent on our ability to increase levels of user engagement, as measured by timeline views and timeline views per MAU, and monetization, as measured by advertising revenue per timeline view. User Engagement. We broadly measure user engagement on our platform through timeline views and the number of timeline views per MAU. In the three months ended June 30, 2013, timeline views increased 69% and timeline views per MAU increased 17%, compared to the three months ended June 30, 2012. We continue to develop products for our platform, and to develop partnerships globally to increase relevant local content on our platform, with the goal of increasing our user engagement. In particular, our most engaged users are generally those who access Twitter via our mobile applications. In the three months ended June 30, 2013, a substantial majority of timeline views were on mobile devices, and the increase in timeline views was driven by mobile user engagement. We expect this trend to continue in the near term, and we plan to continue to develop and improve our mobile applications to further drive user adoption of these applications. However, to the extent user engagement as measured by timeline views and timeline views per MAU does not increase, our revenue growth will depend in large part on our ability to increase MAUs or monetization of our platform. Monetization. We measure monetization of our platform through advertising revenue per timeline view. There are many variables that impact timeline views and advertising revenue per timeline view, such as the number of MAUs, the number of timeline views per MAU, which timeline views we monetize and the amount of advertising we choose to display, our users’ engagement with our Promoted Products and advertiser demand. Generally, for our pay-for-performance Promoted Products, we design our algorithms to optimize for the combined impact of a number of factors, including the overall user experience, the number of ads we deliver to a particular user, the likelihood that our users will engage with the ads, the value we deliver to advertisers and the impact of the advertisers’ bids. We design our algorithms to enhance the user experience by delivering relevant ads to a user based on the user’s Interest Graph, and these ads may contain information of interest to the user or may provide promotional offers that are not available anywhere else. Our algorithms also enhance the value that we deliver to advertisers because the targeting capabilities of our algorithms allow advertisers to deliver ads that are relevant to a user’s interests, thereby increasing the effectiveness of an advertiser’s advertising campaign. We regularly refine our algorithms to drive monetization while maximizing the long-term value of our platform for our users and advertisers. Given the large number of variables that drive advertising revenue per timeline view, including decisions that we make regarding optimizing user experience and satisfying advertiser demand, certain individual components may decline while others increase. Ultimately, it is the combination of the changes in these components that impacts advertising revenue per timeline view. For example, advertising revenue has increased sequentially in each of the five quarters ended June 30, 2013, driven by sequential increases in paid user 64

Table of Contentsengagements with our pay-for-performance Promoted Products, or ad engagements, over those same periods, partially offset by sequential decreases in average cost per ad engagement during the same periods. The number of ad engagements increased 55%, 32%, 78%, 15% and 124% sequentially in the three months ended June 30, 2012, September 30, 2012, December 31, 2012, March 31, 2013 and June 30, 2013, respectively. The increases in ad engagements over these periods were primarily due to increases in MAUs, user engagement levels, as measured by timeline views per MAU, and advertiser demand. Average cost per ad engagement decreased 18%, 9%, 19%, 12% and 46% sequentially in the three months ended June 30, 2012, September 30, 2012, December 31, 2012, March 31, 2013 and June 30, 2013, respectively. The decreases in cost per ad engagement over these periods were primarily due to an increase in supply of advertising inventory available in our auctions, which was partially offset by increased demand for our Promoted Products. Supply of advertising inventory increased as we expanded the distribution of our Promoted Products to our mobile applications and additional markets outside of the United States in 2012. The increase in advertising inventory provided us with additional opportunities to place ads on our platform. This increase in advertising inventory combined with efforts in the three months ended June 30, 2013 to improve the advertiser experience by refining our algorithms to balance the distribution of an advertiser’s budget throughout the day reduced the amount that advertisers were required to bid to win auctions for our pay-for-performance Promoted Products. This reduction in cost per ad engagement made our Promoted Products more attractive for our existing advertisers and new advertisers, including small and medium sized businesses with smaller advertising budgets, as well as international advertisers. As we continue to optimize for advertiser value and the overall user experience, the cost per ad engagement may continue to decline over time, and we expect the cost per ad engagement to decline in the near term. In the event that cost per ad engagement continues to decline, and we are unable to continue to offset the impact of such decreases on advertising revenue by increasing the number of ad engagements, our advertising revenue would decline. We believe that, in order to increase the cost per ad engagement, we will need to increase advertiser demand for our Promoted Products by enhancing the value of such products. We plan to increase the value of our Promoted Products by increasing the size and engagement of our user base, improving our ability to target advertising to our users’ interests and improving the ability of our advertisers to optimize their campaigns and measure the results of their campaigns. We also believe our goal of maximizing the long-term value of our platform for our users and advertisers should make Promoted Products more attractive to our existing and new advertisers and allow us to deliver more relevant ads on our platform. In addition, our advertising revenue per timeline view in the United States is substantially higher than our advertising revenue per timeline view in the rest of the world. For example, during the three months ended June 30, 2013, our advertising revenue per timeline view in the United States was $2.17 and our advertising revenue per timeline view in the rest of the world was $0.30. We expect this disparity to continue for the foreseeable future. Accordingly, to the extent the number of international users and engagement by international users grow faster than U.S. users and engagement by U.S. users, total advertising revenue per timeline view may be adversely impacted even if total advertising revenue continues to increase. We have also been able to generate significant revenue through our mobile applications. We introduced Promoted Products on our iOS and Android mobile applications in February 2012, and have since expanded to include Promoted Products on our other mobile applications. In the three months ended June 30, 2013, over 65% of our advertising revenue was generated from mobile devices. We have experienced strong growth in advertising revenue from mobile devices because user engagement, as measured by timeline views, is significantly higher on mobile applications than on our desktop applications, and we expect this trend to continue. However, Promoted Accounts and Promoted Trends receive less prominence on our mobile applications than they do on our desktop applications, which means that fewer users see them displayed on our mobile applications, resulting in fewer ad engagements with Promoted Accounts and fewer impressions of Promoted 65

Table of ContentsTrends on mobile applications. Primarily as a result of Promoted Accounts and Promoted Trends receiving less prominence on mobile applications, we have generated higher advertising revenue per timeline view on our desktop applications than on our mobile applications. Although advertising revenue per timeline view on our desktop applications is higher than advertising revenue per timeline view on our mobile applications, the substantial majority of our timeline views and advertising revenue is generated from mobile applications. Accordingly, to the extent that user engagement on mobile applications continues to increase faster than user engagement on our desktop applications, advertising revenue per timeline view may be adversely impacted even if total advertising revenue continues to increase. We intend to continue to increase the monetization of our platform by improving the targeting capabilities of our advertising services to enhance the value of our Promoted Products for advertisers, expanding our sales efforts to reach advertisers in additional international markets, opening our platform to additional advertisers through our self-serve advertising platform and developing new ad formats for advertisers. Effectiveness of Our Advertising Services. Advertisers can use Twitter to communicate directly with their followers for free, but many choose to purchase our advertising services to reach a broader audience and further promote their brands, products and services. We believe that increasing the effectiveness of our Promoted Products for advertisers will increase the amount that advertisers spend with us. We aim to increase the value of our Promoted Products by increasing the size and engagement of our user base, improving our ability to target advertising to our users’ interests and improving the ability of our advertisers to optimize their campaigns and measure the results of their campaigns. We may also develop new advertising products and services. International Expansion. We intend to invest in our international operations in order to expand our user base and advertiser base and increase user engagement and monetization internationally. In the three months ended June 30, 2013, we had 169.1 million average MAUs internationally compared to 49.2 million average MAUs in the United States. In addition, our number of users is growing at a faster rate in many international markets, such as Argentina, France, Japan, Russia, Saudi Arabia and South Africa. However, we derive the substantial majority of our advertising revenue from advertisers in the United States. We also generate significantly more advertising revenue per timeline view in the United States than internationally, with advertising revenue per timeline view in the three months ended June 30, 2013 of $2.17 in the United States and $0.30 internationally. Further, because we record advertising revenue based on the billing location of our advertisers, engagement by international users with ads placed by advertisers located in the United States increases our advertising revenue per timeline view in the United States. In order to increase our international advertising revenue, we plan to invest in our international operations. In the near term, we plan to increase the size of our sales and marketing support teams in Australia, Brazil, Ireland and the Netherlands, and we plan to extend our self-serve advertising platform to countries outside of the United States. We face challenges in increasing our advertising revenue internationally, including local competition, differences in advertiser demand, differences in the digital advertising market and conventions, and differences in the manner in which Twitter is accessed and used internationally. We face competition from well established competitors in certain international markets, including Kakao in South Korea and LINE in Japan. In addition, certain international markets are not as familiar with digital advertising in general, or with new forms of digital advertising, such as our Promoted Products. In these jurisdictions we are investing to educate advertisers about the benefits of our advertising services. However, we expect that it may require a significant investment of time and resources to educate advertisers in many international markets. We also face challenges in providing certain advertising products, features or analytics in certain international markets, such as the European Union, due to government regulation. In addition, in certain emerging markets, many users access 66

Table of ContentsTwitter through feature phones with limited functionality, rather than through smartphones, our website or desktop applications. This limits our ability to deliver certain features to these users and may limit the ability of advertisers to deliver compelling ads to users in these markets. We are investing to improve our applications for feature phones in order to improve our ability to monetize our products and services in international markets. Competition. We face significant competition for users and advertisers. We compete against many companies to attract and engage users and for advertiser spend, including companies with greater financial resources and substantially larger user bases, such as Facebook (including Instagram), Google, LinkedIn, Microsoft and Yahoo!, which offer a variety of Internet and mobile device-based products, services and content. In recent years there have been significant acquisitions and consolidation by and among our actual and potential competitors. We must compete effectively for users and advertisers in order to grow our business and increase our revenue. We believe that our ability to compete effectively for users depends upon a number of factors, including the quality of our products and services; and our ability to compete effectively for advertisers depends upon a number of factors, including our ability to offer attractive advertising products with unique targeting capabilities and the size of our active user base. We intend to continue to invest in research and development to improve our products and services for users and advertisers and to grow our active user base in order to address the competitive challenges in our industry. As part of our strategy to improve our products and services, we may acquire other companies to add engineering talent or complementary products and technologies. Investment in Infrastructure. We intend to increase the capacity and enhance the capability and reliability of our infrastructure. Our infrastructure is critical to providing users, platform partners, advertisers and data partners access to our platform, particularly during major planned and unplanned events, such as elections, sporting events or natural disasters, when activity on our platform increases dramatically. As our user base and the activity on our platform grow, we expect that investments and expenses associated with our infrastructure will continue to grow. These investments and expenses include the expansion of our data center operations and related operating costs, additional servers and networking equipment to increase the capacity of our infrastructure and increased bandwidth costs. Products and Services Innovation. Our ability to increase the size and engagement of our user base, attract advertisers and increase our revenue will depend, in part, on our ability to improve existing products and services and to successfully develop or acquire new products and services. We plan to continue to make significant investments in research and development and, from time to time, we may acquire companies to enhance our products, services and technical capabilities. Investment in Talent. We intend to invest in hiring and retaining talented employees to grow our business and increase our revenue. As of June 30, 2013, we had approximately 2,000 full-time employees, an increase of over 900 full-time employees, or approximately 90%, from June 30, 2012. We expect to grow headcount for the foreseeable future as we continue to invest in our business. We have also made and intend to continue to make acquisitions that add engineers, designers, product managers and other personnel with specific technology expertise. In addition, we must retain our high-performing personnel in order to continue to develop, sell and market our products and services and manage our business. Seasonality. Advertising spending is traditionally strongest in the fourth quarter of each year. Historically, this seasonality in advertising spending has affected our quarterly results, with higher sequential advertising revenue growth from the third quarter to the fourth quarter compared to sequential advertising revenue growth from the fourth quarter to the subsequent first quarter. For example, our advertising revenue increased 63% and 45% between the third and fourth quarters of 2011 and 2012, respectively, while advertising revenue for the first quarter of 2012 and 2013 increased 37% and 1% compared to the fourth quarter of 2011 and 2012, respectively. In addition, advertising 67

Table of Contentsrevenue per timeline view increased 31% between the third and fourth quarter of 2012, while advertising revenue per timeline view decreased 13% between the fourth quarter of 2012 and the first quarter of 2013. The rapid growth in our business may have partially masked seasonality to date and the seasonal impacts may be more pronounced in the future. Stock-Based Compensation Expense. Since May 2011, we have been granting RSUs to our employees. The Pre-2013 RSUs vest upon the satisfaction of both a service condition and a performance condition. The service condition for a majority of the Pre-2013 RSUs is satisfied over a period of four years. The performance condition will be satisfied on the earlier of (i) the date that is the earlier of (x) six months after the effective date of this offering or (y) March 8th of the calendar year following the effective date of this offering (which we may elect to accelerate to February 15th); and (ii) the date of a change in control. As of June 30, 2013, no stock-based compensation expense had been recognized for the Pre-2013 RSUs because a qualifying event as described above was not probable. In the quarter in which this offering is completed, we will begin recording stock-based compensation expense based on the grant-date fair value of the Pre-2013 RSUs using the accelerated attribution method, net of estimated forfeitures. If this offering had been completed on June 30, 2013, we would have recorded $329.6 million of cumulative stock-based compensation expense related to the Pre-2013 RSUs on that date, and an additional $234.2 million of unrecognized stock-based compensation expense related to the Pre-2013 RSUs, net of estimated forfeitures, would be recognized over a weighted-average period of approximately three years. In addition to stock-based compensation expense associated with the Pre-2013 RSUs, as of June 30, 2013, we had unrecognized stock-based compensation expense of approximately $296.7 million related to other outstanding equity awards, after giving effect to estimated forfeitures, which we expect to recognize over a weighted-average period of approximately four years. Further, we made grants of equity awards after June 30, 2013, and we have unrecognized stock-based compensation expense of $452.9 million related to such equity awards, after giving effect to estimated forfeitures, which we expect to recognize over a weighted-average period of approximately four years. On the settlement dates for the Pre-2013 RSUs, we may choose to allow our employees who are not executive officers to sell shares of our common stock received upon the vesting and settlement of the Pre-2013 RSUs in the public market to satisfy their income tax obligations related to the vesting and settlement of such awards, or we may choose to undertake a net settlement of these awards and withhold and remit income taxes on behalf of the holders of Pre-2013 RSUs at the applicable minimum statutory rates. We expect the applicable minimum statutory rates to be approximately 40% on average, and the income taxes due would be based on the then-current value of the underlying shares of our common stock. Based on the number of Pre-2013 RSUs outstanding as of June 30, 2013 for which the service condition had been satisfied on that date, and assuming (i) the performance condition had been satisfied on that date and (ii) that the price of our common stock at the time of settlement was equal to $ , which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, we estimate that this tax obligation on the initial settlement date would be approximately $ in the aggregate. The amount of this obligation could be higher or lower, depending on the price of shares of our common stock on the initial settlement date for the Pre-2013 RSUs. To settle these Pre-2013 RSUs on the initial settlement date, assuming a 40% tax withholding rate, if we choose to undertake a net settlement of all of these awards rather than allowing our employees who are not executive officers to sell shares of our common stock in the public market to satisfy their income tax obligations related to the vesting and settlement of such awards, we would expect to deliver an aggregate of approximately shares of our common stock to Pre-2013 RSU holders and withhold an aggregate of approximately shares of our common stock. In connection with these net settlements, we would withhold and remit the tax liabilities on behalf of the Pre-2013 RSU holders to the relevant tax authorities in cash. 68

Table of ContentsComponents of Results of Operations Revenue We generate the substantial majority of our revenue from the sale of advertising services. We also generate revenue by licensing our data to third parties. Advertising Services We generate substantially all of our advertising revenue by selling our Promoted Products. Currently, our Promoted Products consist of the following:

| | Ÿ | | Promoted Tweets. Promoted Tweets, which are labeled as “promoted,” appear within a user’s timeline or search results just like an ordinary Tweet regardless of device, whether it be desktop or mobile. Using our proprietary algorithms and understanding of the interests of each user, we can deliver Promoted Tweets that are intended to be relevant to a particular user. We enable our advertisers to target an audience based on our users’ Interest Graphs. Our Promoted Tweets are pay-for-performance advertising that are priced through an auction. We recognize advertising revenue when a user engages with a Promoted Tweet. |

| | Ÿ | | Promoted Accounts. Promoted Accounts, which are labeled as “promoted,” appear in the same format and place as accounts suggested by our Who to Follow recommendation engine. Promoted Accounts provide a way for our advertisers to grow a community of users who are interested in their business, products or services. Our Promoted Accounts are pay-for-performance advertising that are priced through an auction. We recognize advertising revenue when a user follows a Promoted Account. |

| | Ÿ | | Promoted Trends. Promoted Trends, which are labeled as “promoted,” appear at the top of the list of trending topics for an entire day in a particular country or on a global basis. When a user clicks on a Promoted Trend, search results for that trend are shown in a timeline and a Promoted Tweet created by the advertiser is displayed to the user at the top of those search results. We sell our Promoted Trends on a fixed-fee-per-day basis. We feature one Promoted Trend per day per geography, and recognize advertising revenue from a Promoted Trend when it is displayed on our platform. |

Data Licensing We offer data licenses that allow our data partners to access, search and analyze historical and real-time data on our platform, which data consists of public Tweets and their content. Our data partners generally purchase licenses to access all or a portion of our data for a fixed period, which is typically two years. We recognize data licensing revenue as the licensed data is made available to our data partners. In the six months ended June 30, 2013, our top five data partners accounted for approximately 75% of our data licensing revenue, and approximately 10% of total revenue in the period. We expect data licensing revenue to decrease as a percentage of our total revenue over time. Cost of Revenue and Operating Expenses Cost of Revenue Cost of revenue consists primarily of data center costs related to our co-located facilities, which include lease and hosting costs, related support and maintenance costs and energy and bandwidth costs, as well as depreciation of our servers and networking equipment, and personnel-related costs, including salaries, benefits and stock-based compensation, for our operations teams. Cost of revenue also includes allocated facilities and other supporting overhead costs, amortization of acquired intangible assets and capitalized labor costs. Many of the elements of our cost of revenue are relatively fixed, and cannot be reduced in the near term to offset any decline in our revenue. 69

Table of ContentsWe plan to continue increasing the capacity and enhancing the capability and reliability of our infrastructure to support user growth and increased activity on our platform. We anticipate a significant increase in cost of revenue in the year ending December 31, 2013 as a result of the stock-based compensation expense associated with the Pre-2013 RSUs as described in “—Factors Affecting Our Future Performance—Stock-Based Compensation Expense.” We expect that cost of revenue will increase in dollar amount for the foreseeable future and vary in the near term from period to period as a percentage of revenue. Research and Development Research and development expenses consist primarily of personnel-related costs, including salaries, benefits and stock-based compensation, for our engineers and other employees engaged in the research and development of our products and services. In addition, research and development expenses include allocated facilities and other supporting overhead costs. We plan to continue to hire employees for our engineering, product management and design teams to support our research and development efforts. We anticipate a significant increase in research and development expenses in the year ending December 31, 2013 as a result of the stock-based compensation expense associated with the Pre-2013 RSUs as described in “—Factors Affecting Our Future Performance—Stock-Based Compensation Expense.” We expect that research and development costs will increase in dollar amount for the foreseeable future and vary in the near term from period to period as a percentage of revenue. Sales and Marketing Sales and marketing expenses consist primarily of personnel-related costs, including salaries, benefits and stock-based compensation for our employees engaged in sales, sales support, commissions, business development and media, marketing, corporate communications and customer service functions. In addition, marketing and sales-related expenses also include market research, tradeshows, branding, marketing and public relations costs, as well as allocated facilities and other supporting overhead costs. We plan to continue to invest in sales and marketing to expand internationally, grow our advertiser base and increase our brand awareness. We anticipate a significant increase in sales and marketing expenses in the year ending December 31, 2013 as a result of the stock-based compensation expense associated with the Pre-2013 RSUs as described in “—Factors Affecting Our Future Performance—Stock-Based Compensation Expense.” We expect that sales and marketing expenses will increase in dollar amount for the foreseeable future and vary in the near term from period to period as a percentage of revenue. General and Administrative General and administrative expenses consist primarily of personnel-related costs, including salaries, benefits and stock-based compensation, for our executive, finance, legal, information technology, human resources and other administrative employees. In addition, general and administrative expenses include fees and costs for professional services, including consulting, third-party legal and accounting services and facilities and other supporting overhead costs that are not allocated to other departments. We plan to continue to expand our business both domestically and internationally, and expect to increase the size of our general and administrative function to help grow our business. We expect that we will incur additional general and administrative expenses as a result of being a publicly-traded company. 70

Table of ContentsWe also anticipate a significant increase in general and administrative expenses in the year ending December 31, 2013 as a result of the stock-based compensation expense associated with the Pre-2013 RSUs as described in “—Factors Affecting Our Future Performance—Stock-Based Compensation Expense.” We expect that general and administrative expenses will increase in dollar amount for the foreseeable future and vary in the near term from period to period as a percentage of revenue. Provision (Benefit) for Income Taxes Provision for income taxes consists of federal and state income taxes in the United States and income taxes in certain foreign jurisdictions, and deferred income taxes and changes in related valuation allowance reflecting the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes. As of December 31, 2012, we had $298.8 million of federal and $216.7 million of state net operating loss carryforwards available to reduce future taxable income. These net operating loss carryforwards will begin to expire for federal income tax purposes and state income tax purposes in 2027 and 2017, respectively. We expect our net operating loss carryforwards to increase in the quarter in which we initially settle a portion of the Pre-2013 RSUs as a result of the vesting of such RSUs. We also have research credit carryforwards of $6.6 million and $10.5 million for federal and state income tax purposes, respectively. The federal research credit carryforward will begin to expire in 2027. The state research credit carryforward has no expiration date. Utilization of the net operating loss carryforwards and research carryforwards credit may be subject to an annual limitation due to the ownership change limitations set forth in the Code, and similar state provisions. Any annual limitation may result in the expiration of net operating losses and research credits before utilization. Results of Operations The following tables set forth our consolidated statement of operations data for each of the periods presented:

| | | | | | | | | | | | | | | | | | | | | | | | Year Ended December 31, | | | Six Months Ended

June 30, | | | | | 2010 | | | 2011 | | | 2012 | | | 2012 | | | 2013 | | | | | (In thousands) | | | | | | | | | | | | | | (Unaudited) | | Revenue | | | | | | | | | | | | | | | | | | | | | Advertising services | | $ | 7,321 | | | $ | 77,710 | | | $ | 269,421 | | | $ | 101,302 | | | $ | 221,432 | | Data licensing | | | 20,957 | | | | 28,603 | | | | 47,512 | | | | 21,057 | | | | 32,203 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Total revenue | | $ | 28,278 | | | $ | 106,313 | | | $ | 316,933 | | | $ | 122,359 | | | $ | 253,635 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Costs and expenses(1) | | | | | | | | | | | | | | | | | | | | | Cost of revenue | | | 43,168 | | | | 61,803 | | | | 128,768 | | | | 58,157 | | | | 91,828 | | Research and development | | | 29,348 | | | | 80,176 | | | | 119,004 | | | | 46,345 | | | | 111,837 | | Sales and marketing | | | 6,289 | | | | 25,988 | | | | 86,551 | | | | 34,105 | | | | 77,697 | | General and administrative | | | 16,952 | | | | 65,757 | | | | 59,693 | | | | 30,758 | | | | 35,096 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Total costs and expenses | | | 95,757 | | | | 233,724 | | | | 394,016 | | | | 169,365 | | | | 316,458 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Loss from operations | | | (67,479 | ) | | | (127,411 | ) | | | (77,083 | ) | | | (47,006 | ) | | | (62,823 | ) | Interest income (expense), net | | | 55 | | | | (805 | ) | | | (2,486 | ) | | | (890 | ) | | | (2,746 | ) | Other income (expense), net | | | (117 | ) | | | (1,530 | ) | | | 399 | | | | (12 | ) | | | (2,548 | ) | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Loss before income taxes | | | (67,541 | ) | | | (129,746 | ) | | | (79,170 | ) | | | (47,908 | ) | | | (68,117 | ) | Provision (benefit) for income taxes | | | (217 | ) | | | (1,444 | ) | | | 229 | | | | 1,196 | | | | 1,134 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Net loss | | $ | (67,324 | ) | | $ | (128,302 | ) | | $ | (79,399 | ) | | $ | (49,104 | ) | | $ | (69,251 | ) | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| |

(1) | Costs and expenses include stock-based compensation expense as follows: |

71

Table of Contents | | | | | | | | | | | | | | | | | | | | | | | | Year Ended December 31, | | | Six Months Ended

June 30, | | | | | 2010 | | | 2011 | | | 2012 | | | 2012 | | | 2013 | | | | | (In thousands) | | | | | | | | | | | | | | (Unaudited) | | Cost of revenue | | $ | 200 | | | $ | 1,820 | | | $ | 800 | | | $ | 420 | | | $ | 1,955 | | Research and development | | | 3,409 | | | | 33,559 | | | | 12,622 | | | | 6,291 | | | | 24,197 | | Sales and marketing | | | 249 | | | | 1,553 | | | | 1,346 | | | | 620 | | | | 4,614 | | General and administrative | | | 2,073 | | | | 23,452 | | | | 10,973 | | | | 8,796 | | | | 4,802 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Total | | $ | 5,931 | | | $ | 60,384 | | | $ | 25,741 | | | $ | 16,127 | | | $ | 35,568 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| |

The following table sets forth our consolidated statement of operations data for each of the periods presented as a percentage of revenue:

| | | | | | | | | | | | | | | | | | | | | | | | Year Ended

December 31, | | | Six Months

Ended

June 30, | | | | | 2010 | | | 2011 | | | 2012 | | | 2012 | | | 2013 | | Revenue | | | | | | | | | | | | | | | | | | | | | Advertising services | | | 26 | % | | | 73 | % | | | 85 | % | | | 83 | % | | | 87 | % | Data licensing | | | 74 | | | | 27 | | | | 15 | | | | 17 | | | | 13 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Total Revenue | | | 100 | | | | 100 | | | | 100 | | | | 100 | | | | 100 | | Costs and expenses | | | | | | | | | | | | | | | | | | | | | Cost of revenue | | | 153 | | | | 58 | | | | 41 | | | | 48 | | | | 36 | | Research and development | | | 104 | | | | 75 | | | | 38 | | | | 38 | | | | 44 | | Sales and marketing | | | 22 | | | | 24 | | | | 27 | | | | 28 | | | | 31 | | General and administrative | | | 60 | | | | 62 | | | | 19 | | | | 25 | | | | 14 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Total costs and expenses | | | 339 | | | | 220 | | | | 124 | | | | 138 | | | | 125 | | | |

|

| | |

|

| | |

|

| | |

|

| | |

|

| | Loss from operations | | | (239 | ) | | | (120 | ) | | | (24 | ) | | | (38 | ) | | | (25 | ) | Interest income (expense), net | | | — | | | | (1 | ) | | | (1 | ) | | | (1 | ) | | | (1 | ) | Other income (expense), net | | | — | | | | (1 | ) | | | — | | | | — | | | | (1 | ) | | |

|

| | |

|

| | |

|

| | |